Retirement Account Allocation Strategies for Married Partners

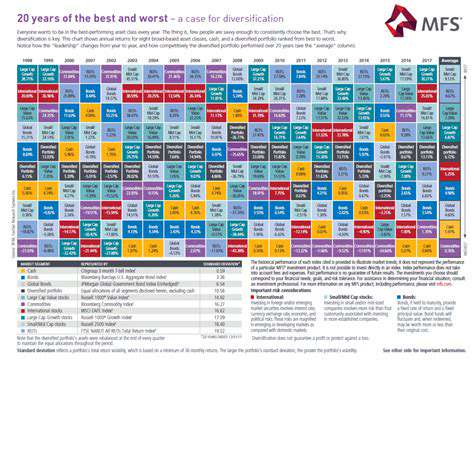

Diversification is a cornerstone of risk management. By spreading your investments across various asset classes, you mitigate the impact of a single investment performing poorly. This strategy involves allocating capital among stocks, bonds, real estate, or other assets. Each asset class exhibits different characteristics and behaviors in the market, leading to a potential reduction in overall portfolio volatility. This is crucial because market conditions are constantly changing, and diversification is an insurance policy for a more stable return.

The Role of Asset Allocation

Asset allocation is the process of strategically distributing your investments across different asset classes based on your risk tolerance and financial goals. It's a fundamental aspect of portfolio construction, determining the proportion of your investment portfolio dedicated to stocks, bonds, and other asset types.

By allocating specific percentages to each asset class, you are actively positioning yourself to capitalize on potential opportunities while controlling the level of risk exposure. Understanding and optimizing this allocation is a proactive approach to achieving long-term financial objectives.

Considering Time Horizon

The time horizon for your investments is a vital component in determining your appropriate allocation. A longer time horizon generally allows for greater risk-taking, as you have more time to recover from potential market downturns. This is because you have the time to reinvest any losses. A shorter time horizon, like a specific future goal, necessitates a more conservative approach to reduce the potential for loss.

Adapting to Market Changes

The investment landscape is dynamic, and your allocation strategy should be adaptable to changing market conditions. Regular portfolio reviews are essential to ensure your investments remain aligned with your current risk tolerance, goals, and economic circumstances. Market trends and economic factors are significant considerations that require vigilance and potentially re-balancing your portfolio.

Periodic review is paramount to maintaining a portfolio that effectively reflects your evolving needs and the market landscape. Be prepared to adjust your allocation as your circumstances and the market evolve.

Leveraging Tax-Advantaged Accounts Effectively

Retirement Accounts: A Powerful Tool

Retirement accounts, such as 401(k)s and IRAs, offer significant tax advantages that can substantially boost your savings for retirement. These accounts allow you to contribute pre-tax dollars, meaning the money you contribute isn't taxed immediately. This deferral of taxes can significantly increase your overall returns over time.

Furthermore, the earnings within these accounts also grow tax-deferred. This compounding effect over the years can lead to a substantial nest egg, making retirement more comfortable and secure. Maximizing contributions to retirement accounts is a crucial step in achieving financial freedom. Properly utilizing these accounts is key to a secure financial future.

Health Savings Accounts (HSAs): A Double Benefit

HSAs are specifically designed for medical expenses, providing a significant tax advantage. You contribute pre-tax dollars to an HSA, and any earnings are not taxed when used for qualified medical expenses. This can lead to substantial savings on medical bills.

This double benefit makes HSAs exceptionally attractive for individuals who anticipate substantial future medical expenses or are looking for a tax-advantaged way to save for those expenses. Contributing regularly to an HSA can significantly reduce your tax burden and provide a financial safety net.

Education Savings Plans: Securing a Child's Future

Education savings plans, commonly known as 529 plans, allow you to set aside money for your children's education. These plans offer tax benefits both on contributions and earnings, making them a powerful tool to help finance college or other post-secondary education expenses. Often, 529 plans permit a range of investments to grow funds for the future.

Whether it's tuition, fees, room and board, or other educational costs, 529 plans can offer significant long-term savings. These plans are a valuable investment tool, not just for financing education, but also for building a strong financial future for your family. Using these plans can potentially lessen the financial burden of education.

Tax-Advantaged Accounts for Small Business Owners

Small business owners have access to a variety of tax-advantaged accounts to help manage their finances and grow their enterprises. These accounts often allow for tax-deductible contributions and potentially tax-deferred growth, streamlining expenses and potentially maximizing profitability. The potential tax savings can be substantial for small business owners.

Utilizing Tax Credits and Deductions

Beyond accounts, various tax credits and deductions can also provide significant financial advantages. Understanding and properly utilizing these credits and deductions can significantly reduce your overall tax liability. Federal, state, and local tax authorities publish information on these available opportunities to help consumers manage finances effectively.

Properly understanding and taking advantage of tax credits and deductions can be a game changer when it comes to managing your personal finances, potentially saving you substantial amounts of money. Remember to consult with a tax professional for personalized guidance.

Seeking Professional Financial Advice

Understanding Retirement Account Types

When planning for retirement, it's essential to understand the various types of accounts available, including 401(k)s, IRAs, and Roth IRAs. Each has its own set of rules regarding contributions, withdrawals, and tax implications that can significantly impact your retirement strategy.

Additionally, some accounts may offer employer matching contributions, which can effectively boost your retirement savings. By understanding how these accounts function and their respective benefits, you can tailor your investment strategy for maximum returns.

The Importance of Asset Allocation

Asset allocation is a fundamental concept in retirement planning that involves diversifying your investments across different asset classes, such as stocks, bonds, and commodities. The right mix will depend on various factors, including your risk tolerance, investment goals, and time horizon until retirement.

Effective asset allocation can help mitigate risks while maximizing returns, ensuring that your retirement funds grow steadily over time. Regularly reviewing and adjusting your portfolio as you age or as market conditions change is essential to stay on track toward your retirement savings goals.

Target Date Funds: A Hands-Off Approach

Target date funds are designed to simplify retirement investing by automatically adjusting the asset allocation based on a selected retirement date. These funds start with a more aggressive investment strategy when you are further from retirement and gradually shift to a conservative allocation as the date approaches.

Many investors appreciate target date funds for their ease of use, as they allow for a more hands-off investment approach. However, it's still important to monitor their performance and fees, ensuring they align with your overall financial goals and expectations for retirement savings.

Tax Implications of Retirement Accounts

Understanding the tax implications of different retirement accounts is vital for developing a sound financial strategy. For instance, traditional IRAs and 401(k)s provide tax-deductible contributions, meaning you won’t pay taxes on that money until you withdraw it in retirement.

On the other hand, Roth IRAs are funded with after-tax dollars, allowing for tax-free withdrawals in retirement. Each type of account carries different benefits and restrictions, so consulting with a financial advisor can help you choose the best option for tax efficiency as you approach retirement.

Rebalancing Your Portfolio

Over time, the performance of different investments within your retirement accounts may vary, leading to an imbalanced portfolio. Rebalancing is the process of realigning the weights of the assets in your portfolio by periodically buying or selling investments to maintain your preferred level of asset allocation.

Regular rebalancing not only helps manage risk but also keeps your investment strategy aligned with your long-term retirement goals, ensuring that your asset allocation remains efficient and effective as market conditions fluctuate.

Engaging with a Financial Advisor

Seeking professional financial advice can provide significant benefits when planning your retirement account allocation strategies. A financial advisor can help you create a personalized plan that takes into account your unique financial situation, investment preferences, and retirement aspirations.

A qualified advisor can also offer insights into market trends, potential investment opportunities, and risk management strategies, providing you with the expertise required to navigate the complexities of retirement planning effectively.

Read more about Retirement Account Allocation Strategies for Married Partners